UNITED KINGDOM

(Updated 2014)

1. ENERGY, ECONOMIC AND ELECTRICITY INFORMATION

1.1. General Overview

Note: The content of this section, including Tables 1 and 2, has been removed by the IAEA to better focus the report on nuclear power.

1.2. Energy Information

1.2.1. Estimated Available Energy

Over the past decade, UK oil and gas production has declined at a faster rate than consumption, resulting in the country returning to being a net energy importer in 2004. Oil remains important to the UK’s energy mix, accounting for 36% of the UK’s total primary energy consumption. The UK is a significant producer of natural gas, however, the country increasingly relies on natural gas imports. Natural gas-fired power stations have replaced coal as the principle source of UK power supply.

TABLE 3. RESERVES OF FOSSIL FUELS AND URANIUM AND POTENTIAL RENEWABLE ENERGY

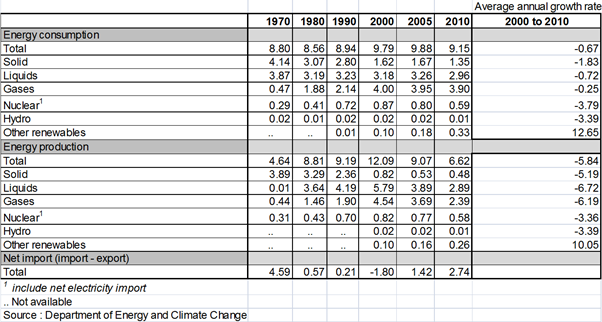

1.2.2. Energy Statistics

In 1970, fuel consumption was dominated by solid fuel use (47% of all energy consumption in the UK) and petroleum (44%), with gas contributing a further 5% and electricity 4%. By 1980, the fuel mix had evolved, with natural gas making up 20% of all energy consumption in the UK, along with solid fuels (36%) and petroleum (37%). In 1990, the split between fuels was similar to that in 1980. However, by 2000, with changes in electricity generation, natural gas consumption had become the dominant fuel, responsible for 41% of all energy consumption in the UK, while solid fuels had fallen from 31% in 1990 to 17% in 2000. By 2010, more renewable fuels had entered the energy mix. Table 4 shows the change in fuel consumption every ten years, between 1970 and 2010.

TABLE 4. ENERGY STATISTICS (EXAJOULES)

1.2.3. Energy Policy

Evidence of potentially damaging man-made climate change has resulted in broad agreement on the need to decarbonise the energy system, while maintaining secure energy supplies at the least cost to consumers. The Government is committed to meeting the legally binding targets to cut greenhouse gas emissions by at least 80% by 2050 and source 15% of energy from renewables by 2020.

Within a market based energy system, and with severe constraints on the public purse, the Government aims to catalyse private sector investment in new infrastructure and in energy efficiency.

Energy Act 2011

The Energy Act provides for some of the key elements of the Coalition’s Programme for Government and its first Annual Energy Statement.

The Act provides for a step-change in the provision of energy efficiency measures to homes and businesses, and makes improvements to our framework to enable and secure low-carbon energy supplies and fair competition in the energy markets.

Energy Act 2013

The Energy Act 2013 establishes a legislative framework for delivering secure, affordable and low-carbon energy. At its core is the need to ensure that, as older power plants are taken offline (a fifth of current capacity within 10 years) and electricity demand continues to increase (it will double over the next 40 years), the UK remains able to generate enough energy to meet its needs. This requires significant investment in new infrastructure to be brought forward – over GBP 100 billion – and new schemes to be integrated, in order to ensure that this investment will contribute to the drive to meet renewables and decarbonisation targets.

The cornerstone of this Act, Electricity Market Reform, includes:

Contracts for Difference – long-term instruments to provide stable and predictable incentives for companies to invest in low-carbon generation;

Final Investment Decisions – to enable early investment in advance of Contracts for Difference;

Capacity Market – to provide security of electricity supply, if required, by ensuring sufficient reliable capacity is available;

Conflicts of Interest and Contingency Arrangements – to ensure the institution which will deliver these two schemes is fit for the purpose;

Renewables Transitional – to ensure that existing investments under the Renewables Obligation remain stable, and

An Emissions Performance Standard – to curb the most-polluting fossil fuel power stations.

The regulatory environment is equally critical to investor confidence when the sums of money are so large (one consortia alone could invest around 20 billion euro in four new nuclear reactors). A coherent and stable regulatory environment minimises costs, creates jobs (Cogent, the Sector Skills Council, estimate that for each power plant there will be 5,000 jobs in construction and 1,000 longer-term operating jobs) and helps keep consumer energy bills low.

The Energy Act improves regulatory certainty by ensuring that Government and Ofgem are aligned at a strategic level through a Strategy and Policy Statement, as recommended in the Ofgem Review of July 2011.

The Act places the Office for Nuclear Regulation (ONR) on a statutory footing as the body to regulate the safety and security of the next generation of nuclear power plants.

1.3. The Electricity and Gas System

1.3.1. Electricity policy and decision making process

With respect to Great Britain (i.e. England, Scotland and Wales), responsibility for energy policy rests with the United Kingdom Government and Parliament. However, energy projects may involve areas of competence that have been devolved to the respective administrations of Scotland and Wales.

Within government, lead responsibility on energy matters outside Northern Ireland rested, until 12 April 1992, with the Secretary of State for Energy. On 13 April 1992, the Secretary of State's responsibilities were transferred to the Secretary of State for Trade and Industry, except for energy efficiency, which was transferred to the Secretary of State for the Environment. On 3 October 2008, responsibility for both was passed to the Secretary of State for Energy and Climate Change, within the newly created Department of Energy and Climate Change.

In Northern Ireland, energy matters and associated issues, such as energy consents and planning, are largely devolved to the Northern Ireland Executive and Assembly. The main exception is nuclear energy, which is dealt with by the UK Government and Parliament.

1.3.2. Structure of electricity power sector

Electricity distribution networks carry electricity from the transmission systems and some generators that are connected to the distribution networks to industrial, commercial and domestic users.

There are 14 licensed distribution network operators (DNOs), each responsible for a distribution services area. The 14 DNOs are owned by six different groups. There are also four independent network operators, who own and run smaller networks embedded in the DNO networks.

Domestic and most commercial consumers buy their electricity from suppliers who pay the DNOs for transporting their customers' electricity along their networks.

The wholesale electricity market in England and Wales was reformed on 27 March 2001, when the Electricity Pool was replaced by New Electricity Trading Arrangements (NETA). This arrangement was extended to Scotland on 1 April 2005 with the introduction of the British Electricity Transmission and Trading Arrangements (BETTA).

The key features of BETTA are:

a forward market where generators are be able to contract with suppliers and large customers for the physical delivery of electricity. Such contracts can be struck close to the time of delivery or a year or more ahead;

two power exchanges (N2EX and APX Endex) to enable participants to refine their contract positions, through day-ahead auctions and continuous trading close to real time, in the light of current information (e.g. on the weather).;

a balancing mechanism, operating from 1 hour ahead of real time up to real time, managed by the National Grid Company (NGC). As electricity cannot be stored, NGC needs to manage the grid system on a second-by-second basis, and the balancing mechanism is the facility under the new arrangements which allows it to do this. However, the vast majority of trading takes place in the forward markets rather than in the Balancing Mechanism;

associated OTC and exchange-based derivatives markets (only on N2EX) to enable market participants to manage commercial risks; and

a settlement process to deal with the financial settlement of balancing mechanism trades, and to deal with those whose generation or consumption of electricity is out of balance with their contracted position.

Transmission Networks

The onshore transmission network is owned by three licensed Transmission Owners (TOs) - National Grid Electricity Transmission (NGET) in England and Wales, Scottish Hydro-Electric Transmission Ltd (SHETL) in Northern Scotland, and Scottish Power Transmission (SPT) in Southern Scotland.

NGET is also National Electricity Transmission System Operator (NETSO), and is responsible for overseeing and managing (balancing) the flow of electricity across the whole of the transmission network. This includes the elements owned and operated by SPT and SHETL. National Grid also co-ordinates connection offers to new generators.

Distribution Networks

There are 14 licensed distribution network operators (DNOs), each responsible for a geographical distribution services area. The 14 DNOs are owned by six different groups.

A new regulatory framework for offshore electricity transmission has been put in place. A key element to this framework is a competitive tender process run by Ofgem, to appoint Offshore Transmission Owners (OFTOs) to construct (where appropriate), own and operate the offshore transmission assets.

In Northern Ireland, all the electricity transmission and distribution lines are owned by Northern Ireland Electricity Ltd (NIE Ltd). The Transmission System Operator is System Operator Northern Ireland (SONI). SONI works in partnership with its counterpart in the Republic of Ireland, EirGrid, to act as the Single Energy Market Operator (SEMO) for the new all-island wholesale market for electricity, established in 2007.

Electricity Generation

Most electricity is generated at large power stations connected to the national transmission network. However, electricity can also be generated in smaller-scale power stations which are connected to the regional distribution networks. The number and type of power station built is the decision of each individual company, based on market signals and government policy on issues such as the environment. There are many companies in the electricity generation sector, from large multinationals to small, family-owned businesses running a single site.

Suppliers buy electricity from generators in the wholesale market and sell it on to customers. Suppliers work in a competitive market, and customers can choose any supplier to provide them with electricity.

Regulation of electricity markets in England, Wales and Scotland is the responsibility of the Gas and Electricity Markets Authority (GEMA), which is bound by statutory duties set out in the Electricity Act 1989. Members of the Authority are appointed by the Secretary of State. The Authority`s principle objective is to protect the interests of consumers.

An application for a new power station with a capacity of over 50 MW in England and Wales requires the consent of the Secretary of State for Energy and Climate (consent powers are devolved in the case of plants in Scotland and Northern Ireland). In England and Wales, applications are made to the Planning Inspectorate (“PINS”) which, once it has accepted the application, will conduct an examination of the application including environmental assessment. Once the examination is complete, PINS will report its conclusions and recommendation to the Secretary of State. The processes of examination, recommendation and decision have defined timescales by which they must be completed.

1.3.3. Main Indicators

In 2010, the energy industries contributed about 3.4% to GDP at basic prices. This is well below the peak level of 10.4%, achieved during the early 1980s. However, since then, energy Gross Value Added (GVA) has grown by an average of 1.9% per year, with the lower share a result of wider growth in the economy.

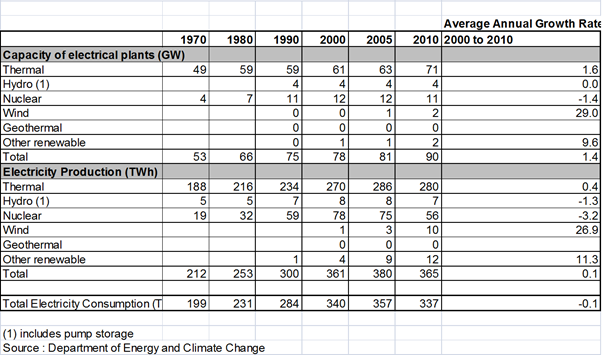

TABLE 5. ELECTRICITY PRODUCTION, CONSUMPTION AND CAPACITY

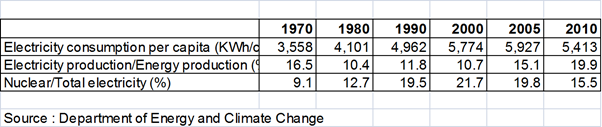

TABLE 6. ENERGY RELATED RATIOS

2. NUCLEAR POWER SITUATION

This report provides an update on the nuclear power situation in the United Kingdom.

2.1. Historical development and current organizational structure

2.1.1. Overview

The United Kingdom (UK) has a wide range of nuclear power plants (NPPs) with a range of designs that span nearly 50 years. The first nuclear power plants, the Magnox reactors, started operation between 1956 and 1971. These are carbon dioxide gas-cooled graphite moderated reactors that use natural (or in some cases very slightly enriched) uranium fuel in a magnesium alloy cladding. The first nine NPPs had steel reactor pressure vessels while the last two (at Oldbury and Wylfa) had pre-stressed concrete reactor pressure vessels. These later designs had significant safety advantages over the steel pressure vessels since a sudden and unexpected failure of the main pressure vessel boundary was deemed to be virtually impossible. However, the use of natural uranium with magnesium alloy cladding limited the development of the Magnox technology regarding increasing power density and gas outlet temperature. As a result, the second generation of gas-cooled reactors to be developed in the UK were the advanced gas cooled reactors (AGR). Seven NPPs were commissioned between 1976 and 1988 each with two reactors. AGRs use enriched uranium oxide fuel in stainless steel cladding. This, together with the pre-stressed concrete pressure vessel, allowed gas outlet temperatures of over 600oC and gas pressures of over 30 bar. The most recent NPP to be built in the UK is the pressure water reactor (PWR) at Sizewell B. The reactor became operational in 1995 and uses enriched uranium oxide fuel clad in Zircalloy and pressurised water as the coolant.

Following a public consultation in 2007, the UK Government published Meeting the Energy Challenge: A White Paper on Nuclear Power1 in January 2008 (the White Paper). The White Paper set out the Government’s view that it was in the public interest to give the private sector the option of investing in new nuclear power stations as part of the UK’s strategy to tackle the challenges of climate change and security of energy supply. The UK considers nuclear energy, together with renewable resources and carbon capture and storage, as key elements to reduce carbon dioxide (CO2) emissions 80% by 2050. This target essentially implies the decarbonisation of the power sector by 2030. It is Government policy that new nuclear power should be able to contribute as much as possible to the UK’s need for new capacity. Energy companies have at present announced ambitions to construct up to 16GW of new nuclear power capacity, with the first station coming on-stream from 2023.

The 2008 White Paper set out the clear division of responsibilities between the public and the private sectors. The Government is responsible for the facilitative actions necessary for new nuclear to go ahead, including institutional and market reforms and defining policies for nuclear waste disposal and decommissioning. Companies will be responsible for the building and operation of new nuclear power stations and for decommissioning and meeting the costs of waste disposal. In October 2010, the Secretary of State for Energy and Climate Change confirmed in Parliament that there would be no public subsidy for new nuclear power stations.

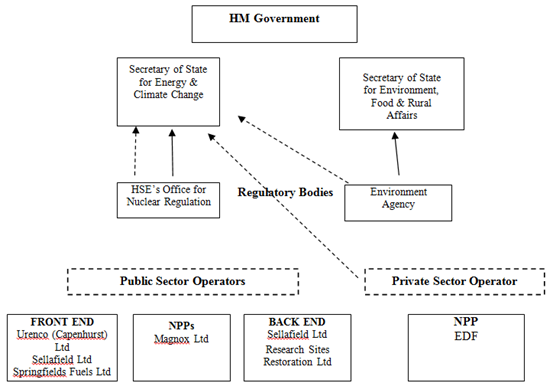

2.1.2. Current organisational chart

A simplified chart of main operations of the United Kingdom nuclear power programme is shown in Figure 1.

Source: DECC

FIGURE 1. UK CURRENT ORGANIZATIONAL STRUCTURE

2.2. Nuclear power plants: Overview

2.2.1. Status and performance of nuclear power plants.

The UK has 19 nuclear licensed sites with NPPs. This includes those sites that are shut down, are defueling or are decommissioning. As at the end of April 2012, there are 16 licensed reactors with a combined capacity of 10 GW still operating in the UK. The largest nuclear operator is EDF Energy UK Ltd, a wholly owned subsidiary of Electricité de France (EDF), which purchased British Energy Group plc in January 2009. It runs eight NPPs, seven of which are the AGRs (a total of 14 reactors) and the remaining plant is the PWR at Sizewell B (one reactor). One Magnox NPP (Wylfa 1 with one reactor) is still in operation and is operated by Magnox Ltd. Table 7 shows the status of the NPPs in the UK up to 30 April 2012. The map at Figure 2 shows the locations of the UK’s NPP sites including those listed by the Government as potentially suitable for new build.

TABLE 7: STATUS OF NUCLEAR POWER PLANTS

| Reactor Unit | Type | Net Capacity [MW(e)] |

Status | Operator | Reactor Supplier |

Construction Date |

First Criticality Date |

First Grid Date |

Commercial Date |

Shutdown Date |

UCF for 2015 |

| DUNGENESS B-1 | GCR | 520 | Operational | EDF UK | APC | 1965-10-01 | 1982-12-23 | 1983-04-03 | 1985-04-01 | 83.5 | |

| DUNGENESS B-2 | GCR | 520 | Operational | EDF UK | APC | 1965-10-01 | 1985-12-04 | 1985-12-29 | 1989-04-01 | 59.7 | |

| HARTLEPOOL A-1 | GCR | 595 | Operational | EDF UK | NPC | 1968-10-01 | 1983-06-24 | 1983-08-01 | 1989-04-01 | 58.8 | |

| HARTLEPOOL A-2 | GCR | 585 | Operational | EDF UK | NPC | 1968-10-01 | 1984-09-09 | 1984-10-31 | 1989-04-01 | 61.3 | |

| HEYSHAM A-1 | GCR | 580 | Operational | EDF UK | NPC | 1970-12-01 | 1983-04-06 | 1983-07-09 | 1989-04-01 | 43.1 | |

| HEYSHAM A-2 | GCR | 575 | Operational | EDF UK | NPC | 1970-12-01 | 1984-06-03 | 1984-10-11 | 1989-04-01 | 49.2 | |

| HEYSHAM B-1 | GCR | 610 | Operational | EDF UK | NPC | 1980-08-01 | 1988-06-23 | 1988-07-12 | 1989-04-01 | 77.2 | |

| HEYSHAM B-2 | GCR | 610 | Operational | EDF UK | NPC | 1980-08-01 | 1988-11-01 | 1988-11-11 | 1989-04-01 | 96.3 | |

| HINKLEY POINT B-1 | GCR | 475 | Operational | EDF UK | TNPG | 1967-09-01 | 1976-09-24 | 1976-10-30 | 1978-10-02 | 93.7 | |

| HINKLEY POINT B-2 | GCR | 470 | Operational | EDF UK | TNPG | 1967-09-01 | 1976-02-01 | 1976-02-05 | 1976-09-27 | 74.0 | |

| HUNTERSTON B-1 | GCR | 475 | Operational | EDF UK | TNPG | 1967-11-01 | 1976-01-31 | 1976-02-06 | 1976-02-06 | 79.9 | |

| HUNTERSTON B-2 | GCR | 485 | Operational | EDF UK | TNPG | 1967-11-01 | 1977-03-27 | 1977-03-31 | 1977-03-31 | 95.5 | |

| SIZEWELL B | PWR | 1198 | Operational | EDF UK | PPC | 1988-07-18 | 1995-01-31 | 1995-02-14 | 1995-09-22 | 100.0 | |

| TORNESS-1 | GCR | 590 | Operational | EDF UK | NNC | 1980-08-01 | 1988-03-25 | 1988-05-25 | 1988-05-25 | 95.5 | |

| TORNESS-2 | GCR | 595 | Operational | EDF UK | NNC | 1980-08-01 | 1988-12-23 | 1989-02-03 | 1989-02-03 | 70.9 | |

| BERKELEY-1 | GCR | 138 | Permanent Shutdown | ML | TNPG | 1957-01-01 | 1961-08-01 | 1962-06-12 | 1962-06-12 | 1989-03-31 | |

| BERKELEY-2 | GCR | 138 | Permanent Shutdown | ML | TNPG | 1957-01-01 | 1962-03-01 | 1962-06-24 | 1962-10-20 | 1988-10-26 | |

| BRADWELL-1 | GCR | 123 | Permanent Shutdown | ML | TNPG | 1957-01-01 | 1961-08-01 | 1962-07-01 | 1962-07-01 | 2002-03-31 | |

| BRADWELL-2 | GCR | 123 | Permanent Shutdown | ML | TNPG | 1957-01-01 | 1962-04-01 | 1962-07-06 | 1962-11-12 | 2002-03-30 | |

| CALDER HALL-1 | GCR | 49 | Permanent Shutdown | SL | UKAEA | 1953-08-01 | 1956-05-01 | 1956-08-27 | 1956-10-01 | 2003-03-31 | |

| CALDER HALL-2 | GCR | 49 | Permanent Shutdown | SL | UKAEA | 1953-08-01 | 1956-12-01 | 1957-02-01 | 1957-02-01 | 2003-03-31 | |

| CALDER HALL-3 | GCR | 49 | Permanent Shutdown | SL | UKAEA | 1955-08-01 | 1958-01-01 | 1958-03-01 | 1958-05-01 | 2003-03-31 | |

| CALDER HALL-4 | GCR | 49 | Permanent Shutdown | SL | UKAEA | 1955-08-01 | 1958-12-01 | 1959-04-01 | 1959-04-01 | 2003-03-31 | |

| CHAPELCROSS-1 | GCR | 48 | Permanent Shutdown | ML | UKAEA | 1955-10-01 | 1958-11-09 | 1959-02-01 | 1959-03-01 | 2004-06-29 | |

| CHAPELCROSS-2 | GCR | 48 | Permanent Shutdown | ML | UKAEA | 1955-10-01 | 1959-05-30 | 1959-07-01 | 1959-08-01 | 2004-06-29 | |

| CHAPELCROSS-3 | GCR | 48 | Permanent Shutdown | ML | UKAEA | 1955-10-01 | 1959-08-31 | 1959-11-01 | 1959-12-01 | 2004-06-29 | |

| CHAPELCROSS-4 | GCR | 48 | Permanent Shutdown | ML | UKAEA | 1955-10-01 | 1959-12-22 | 1960-01-01 | 1960-03-01 | 2004-06-29 | |

| DOUNREAY DFR | FBR | 11 | Permanent Shutdown | UKAEA | UKAEA | 1955-03-01 | 1959-11-14 | 1962-10-01 | 1962-10-01 | 1977-03-01 | |

| DOUNREAY PFR | FBR | 234 | Permanent Shutdown | UKAEA | TNPG | 1966-01-01 | 1974-03-01 | 1975-01-10 | 1976-07-01 | 1994-03-31 | |

| DUNGENESS A-1 | GCR | 225 | Permanent Shutdown | ML | TNPG | 1960-07-01 | 1965-06-01 | 1965-09-21 | 1965-10-28 | 2006-12-31 | |

| DUNGENESS A-2 | GCR | 225 | Permanent Shutdown | ML | TNPG | 1960-07-01 | 1965-09-01 | 1965-11-01 | 1965-12-30 | 2006-12-31 | |

| HINKLEY POINT A-1 | GCR | 235 | Permanent Shutdown | ML | EE/B&W/T | 1957-11-01 | 1964-05-01 | 1965-02-16 | 1965-03-30 | 2000-05-23 | |

| HINKLEY POINT A-2 | GCR | 235 | Permanent Shutdown | ML | EE/B&W/T | 1957-11-01 | 1964-10-01 | 1965-03-19 | 1965-05-05 | 2000-05-23 | |

| HUNTERSTON A-1 | GCR | 150 | Permanent Shutdown | ML | GEC | 1957-10-01 | 1963-08-01 | 1964-02-05 | 1964-02-05 | 1990-03-30 | |

| HUNTERSTON A-2 | GCR | 150 | Permanent Shutdown | ML | GEC | 1957-10-01 | 1964-03-01 | 1964-06-01 | 1964-07-01 | 1989-12-31 | |

| OLDBURY A-1 | GCR | 217 | Permanent Shutdown | ML | TNPG | 1962-05-01 | 1967-08-01 | 1967-11-07 | 1967-12-31 | 2012-02-29 | |

| OLDBURY A-2 | GCR | 217 | Permanent Shutdown | ML | TNPG | 1962-05-01 | 1967-12-01 | 1968-04-06 | 1968-09-30 | 2011-06-30 | |

| SIZEWELL A-1 | GCR | 210 | Permanent Shutdown | ML | EE/B&W/T | 1961-04-01 | 1965-06-01 | 1966-01-21 | 1966-03-25 | 2006-12-31 | |

| SIZEWELL A-2 | GCR | 210 | Permanent Shutdown | ML | EE/B&W/T | 1961-04-01 | 1965-12-01 | 1966-04-09 | 1966-09-15 | 2006-12-31 | |

| TRAWSFYNYDD-1 | GCR | 195 | Permanent Shutdown | ML | APC | 1959-07-01 | 1964-09-01 | 1965-01-14 | 1965-03-24 | 1991-02-06 | |

| TRAWSFYNYDD-2 | GCR | 195 | Permanent Shutdown | ML | APC | 1959-07-01 | 1964-12-01 | 1965-02-02 | 1965-03-24 | 1991-02-04 | |

| WINDSCALE AGR | GCR | 24 | Permanent Shutdown | UKAEA | UKAEA | 1958-11-01 | 1962-08-09 | 1963-02-01 | 1963-03-01 | 1981-04-03 | |

| WINFRITH SGHWR | SGHWR | 92 | Permanent Shutdown | UKAEA | ICL/FE | 1963-05-01 | 1967-09-01 | 1967-12-01 | 1968-01-01 | 1990-09-11 | |

| WYLFA-1 | GCR | 490 | Permanent Shutdown | ML | EE/B&W/T | 1963-09-01 | 1969-11-01 | 1971-01-24 | 1971-11-01 | 2015-12-30 | 76.0 |

| WYLFA-2 | GCR | 490 | Permanent Shutdown | ML | EE/B&W/T | 1963-09-01 | 1970-09-01 | 1971-07-21 | 1972-01-03 | 2012-04-25 |

| Data source: IAEA - Power Reactor Information System (PRIS). | |||||||||||

| Note: Table 7 is completely generated from PRIS data to reflect the latest available information and may be more up to date than the text of the report. |

FIGURE 2. SITES OF EXISTING AND PROPOSED NUCLEAR POWER STATIONS IN THE UK.

Nuclear sites are licensed by the Office for Nuclear Regulation (ONR), the regulator responsible for overseeing their safe operation. The UK has been undertaking safety reviews of its civil nuclear installations for many years as part of the regulatory process. UK nuclear site licences require periodic safety reviews (PSR) to be carried out, which means that the UK continually monitors and aims to improve the safety of its nuclear installations. The main PSRs are carried out every 10 years. However intermediate reviews are carried out at more frequent intervals and any identified necessary upgrading measures are implemented. Additionally, several of the licensees are looking to better integrate the periodic review into enhanced continuous improvement programmes that will deliver improvements throughout the station life.

The majority of the 11 Magnox NPPs had ceased operating by the end of 2006 and are now in various stages of being defueled or decommissioned. A further three (Oldbury A2, Oldbury A1 and Wylfa 2) were shut down between June 2011 and April 2012. The Nuclear Decommissioning Authority (NDA), which was established in 2005, is responsible for a UK wide strategic focus on decommissioning and cleaning up of nuclear sites. In 2011, the NDA published its Strategy5 for delivering the nuclear clean-up programme including the decommissioning the UK’s legacy nuclear plants.

2.2.2. Plant upgrading, plant life management and licence renewals

The UK reactor fleet is comparatively old and this inevitably gives rise to safety related ageing issues that need to be monitored and where necessary addressed. Some ageing issues are controlled and managed by maintenance and replacement of components. Other issues, such as the degradation of the graphite core affect items that cannot be replaced and therefore are closely scrutinised to ensure safety is maintained and, when appropriate, to determine when ageing could lead to the end of life of a reactor.

Operators previously stated that they expected up to 7.4 GW of existing nuclear capacity to close by 2019 (see indicative lifetime dates below). However, as part of their end of year results in 2012 EDF announced that they intend to undertake a programme of investment that will allow their AGR fleet to run for an average of 7 years beyond their previous indicative closure dates, and the PWR at Sizewell B to run for an additional 20 years.

SOURCE: DECC

2.3. Future Development of Nuclear Power

2.3.1. Nuclear power development strategy

The Government has taken a series of facilitative actions to encourage nuclear new build, and industry has proposed investment of up to 16 GW. The first reactor is scheduled to go online in 2023. New nuclear investments will be part of the total GBP 75 billion estimated for new power generation capacity needed by 2020. Three consortia are currently preparing for the construction of new nuclear power plants:

NNB Genco (NNBG) is a joint venture led by EDF. NNBG has plans to build up to 6.4 GW at Hinkley Point in Somerset and Sizewell in Suffolk;

Horizon Nuclear Power, owned by Hitachi-GE Nuclear Energy Ltd, has plans to build up to 6.6 GW at Wylfa in Anglesey and Oldbury in Gloucestershire;

NuGen is a consortium of Toshiba / Westinghouse and Iberdrola. NuGen has plans to build up to 3.6 GW at Moorside near Sellafield in Cumbria;

Among the consortia, NNB has made most progress having received a development consent order (planning permission) from the Department of Energy and Climate Change in March 2013 and regulatory approval (site licence, environmental permits and Generic Design Assessment of its EPR reactor design) in late 2012.

Generic Design Assessment (GDA) is one of the facilitative actions set out in the Nuclear White Paper 20081 and is undertaken by the Office for Nuclear Regulation (ONR) and the Environment Agency. GDA is a voluntary process that allows regulators to begin consideration of the generic safety, security and environmental aspects of designs for NPPs prior to applications for site-specific licence and planning consents.

For new nuclear build, Section 45 of the Energy Act 20086 requires prospective nuclear operators to submit a Funded Decommissioning Programme (FDP) for approval by the Secretary of State for Energy and Climate Change. The Department of Energy and Climate Change published final FDP statutory guidance7 in December 2011 to assist operators to develop their programmes. This will ensure that operators of new nuclear power stations make secure financial provisions for their waste and decommissioning liabilities from the outset.

The Government received an FDP submission from NNB in March 2012. Discussions with NNB are continuing and are expected to be concluded later in 2013.

2.3.2. Project management

Project management will be the responsibility of the commercial developers involved in the new nuclear programme in the UK.

2.3.3. Project funding

New nuclear build in the UK is to be financed and operated by the private sector without public subsidies, including meeting the full costs of decommissioning and their full share of waste management and disposal costs.

2.3.4. Electric grid development

Much of the future of nuclear energy in the UK hinges on the precise conditions of the Government’s announced reform of the electricity and carbon markets to promote low-carbon technologies. The 2011 White Paper Planning Our Electric Future: a White Paper for Secure, Affordable and Low-Carbon Electricity8 spelled out that the key element of the reform would consist of long-term feed-in tariffs (FiT) with contracts for difference (FiT/CfD) which would guarantee low carbon producers (including nuclear power producers) a fixed “strike price” over the contract. Coupled with a gradually rising price floor in the carbon market and a yet-to-be created capacity market, these reforms should make nuclear energy an attractive option for private investors.

The precise arrangements surrounding the contracts for difference are still subject to discussion. These include the level of the strike price; process for setting it, possibly through a tender or an auction; and the institutional arrangements required to handle multi-billion transfers over many years. From the point of view of the operator, the contract-for-difference part of a FiT/CfD is particularly attractive, since it provides financial and legal certainty over long timeframes, especially if coupled with a volume guarantee(1). Standard feed-in tariffs can be revoked through a routine regulatory or legal change, but legally binding private contracts that were cleared by a counter party independent of the UK Treasury would provide a significantly higher degree of certainty.

For the operator, a FiT/CfD is also preferable to a premium FiT (PFiT), which pays the operator a fixed premium over the market price. The PFit stabilises minimum revenue, but not average revenue and leaves a financial downside risk. If wholesale prices rise a FiT/CfD should be able to generate the same risk reduction benefit for the operator at an overall lower financial exposure for the Government. CfDs might also have the beneficial side-effect of allowing for increased competition at all levels of the electricity value chain, since they would remove the need for electricity producers to hedge themselves against wholesale price risk through vertical integration all along the value chain, including retail operations. The UK electricity markets are today dominated by the vertically integrated big six utilities, and the wholesale market is small and illiquid, a configuration that has recently come under increasing scrutiny by the public, politicians and regulators alike.

In the 2011 White Paper, the Government proposes that CfD would be available for all major low-carbon technologies, nuclear, renewables and Carbon Capture and Storage. This measure is deemed necessary to overcome the intrinsic disadvantage of low-carbon technologies in a free-market environment, namely a high ratio of fixed costs to variable costs, which makes such technologies vulnerable to the risk of sudden electricity price changes. Logically FiT/CfDs would only be available for new plants. In the absence of such stabilising measures, natural gas would be the fuel of choice for much of the required new investment, given the price uncertainty in the volatile UK power market. Even a carbon price on its own might not be able to overcome this bias. This in return would pose issues for the security of energy supply. Only the combination of the three main measures of UK electricity market reform – contracts for difference, carbon price floor and capacity market – is deemed to be able to fully internalise the negative externalities of climate change and security of supply risk.

From the point of view of the Government, the CfDs for low-carbon technologies would ideally be technology neutral. However, a first round of bidding will certainly involve differentiated strike prices offered to nuclear, renewables and CCS. In this line-up, nuclear is considered the most cost-effective low-carbon technology, before onshore wind, whereas offshore wind and CCS are considered more expensive. There is hope that the risk reduction inherent in CfDs would also reduce costs of financing low-carbon technologies across the board and that one day, a single CfD tender might be held for all technologies. However, in the near term, CfDs would be required to spur much needed investment. Owing to the pending closure of existing plant, including coal and nuclear plants, de-rated capacity margins will fall from today’s 20% to as low as 5% in some years by the end of the decade.

2.3.5. Site selection

The Government’s National Policy Statement (NPS) for Nuclear Power Generation9 published in July 2011, sets out the UK Government’s policy on the siting of new nuclear power stations. It explains the need for new infrastructure and how the impacts of development should be assessed. The list of potentially suitable sites for the deployment of new nuclear power stations was an output of the Government’s Strategic Siting Assessment (SSA) process. Eight potential sites have been selected all of which are located next to existing nuclear facilities (see Figure 2). Detailed site selection information can be found in the NPS on the Government website at:

https://www.gov.uk/government/publications/national-policy-statements-for-energy-infrastructure

2.4. Organisations involved in construction of NPPs

No new nuclear plants have been constructed in the UK since Sizewell B in the late 1980s. Three consortia are involved in the new build process (as described in 2.3.1 above).

2.5. Organisations involved in the Operation of NPPs

There are 9 operational nuclear power stations in the UK of which 8 are run by EDF and 1 by Magnox Ltd. The remaining shutdown Magnox stations are owned by the NDA.

In 2008 Magnox Electric Ltd separated into two Site Licence Companies; Magnox North Ltd with the sites of; Chapelcross, Hunterston A, Oldbury, Trawsfynydd and Wylfa and Magnox South Ltd with the sites of; Berkeley, Bradwell, Dungeness A, Hinkley Point A and Sizewell A. However, in January 2011 the sites in Magnox South Ltd were relicensed back to Magnox North Ltd. The company was renamed Magnox Ltd and is currently owned by Energy Solutions. This recombination of the sites and associated support provides for a greater organisational resilience and potential benefits from economies of scale. The application to reintegrate was reviewed by the Nuclear Installation Inspectorate at the end of 2010 and their Chief Inspector granted the regulatory permission for the necessary relicensing at the beginning of 2011. A further competition to appoint a single Parent Body Organisation for Magnox Ltd commenced in 2012.

EDF Energy purchased British Energy Group plc in January 2009. Consequently, British Energy was delisted from the London Stock Exchange on 3 February 2009 and became a subsidiary company of EDF Energy UK Ltd. Within British Energy Group there is one nuclear operating company, British Energy Generation Ltd (BEGL). BEGL is the nuclear licensee for Sizewell B, Dungeness B, Hinkley Point B, Heysham 1, Heysham 2, Hartlepool, Hunterston B and Torness. EDF Energy UK Ltd is establishing a new company to become a nuclear licensee for the planned new NPP at Hinkley Point.

2.6. Organisations involved in the Decommissioning of NPPs

The NDA is responsible for providing the first ever UK wide strategic focus on decommissioning and cleaning up nuclear sites. It owns the former nuclear sites and the associated civil nuclear liabilities and assets of the public sector including all the former sites and reactors of British Nuclear Fuels Limited (BNFL) and the UK Atomic Energy Authority (UKAEA). Its responsibilities include decommissioning and clean up of these installations and sites, as well as the implementation of the UK nuclear waste policy.

2.7. Fuel Cycle including Waste Management

Apart from raw uranium mining and uranium ore purification, the UK has an independent nuclear fuel cycle capability. UK - based companies offer a full range of the nuclear fuel cycle services - from uranium conversion, enrichment and fuel manufacture to spent fuel reprocessing, transport, waste management and decommissioning. These services are provided to the UK and international markets.

The nuclear facilities involved in the nuclear fuel cycle in the UK are shown in Figure 1. Uranium enrichment in the UK is carried out at Capenhurst by Urenco UK (UUK) Limited, a wholly owned subsidiary of the Urenco Enrichment Company (UEC) Ltd, which itself is 100% owned by Urenco Ltd. Urenco Ltd is the holding company for the Urenco Group, the joint Anglo-Dutch-German organization which operates uranium enrichment plants in all three countries, and in the USA, using centrifuge technology.

Westinghouse Electric UK Ltd manages the Springfield site, providing nuclear fuel chemical and mechanical fuel fabrication for the UK’s AGR’s, as well as uranium hexafluoride conversion services.

Spent fuel from Magnox and AGRs and overseas Light Water Reactors is reprocessed at the two reprocessing plants at Sellafield. The Thorp plant began operations in March 1994 and has sheared and dissolved over 7000 tonnes of spent fuel. The Magnox reprocessing plant has operated for over 45 years and is scheduled to shut down around 2017-2020 following the closure of the last UK Magnox reactor.

The closure of the Sellafield MOX plant (SMP) was announced in 2011 following limited success in manufacturing MOX fuel for overseas reprocessing customers using a blend of plutonium (recovered from the reprocessing of spent fuel) and uranium.

The Low Level Waste Repository in West Cumbria is licensed for the disposal of Low Level Radioactive Waste (LLW). LLW is transported there by rail or road in purpose designed and licensed containers for disposal in engineered vaults. In addition three landfill sites in Northants, Lillyhall in Cumbria and Peterhead in Scotland were recently granted licenses for the disposal of high volume, low level waste.

In October 2006 the Government accepted the recommendation from the Committee on Radioactive Waste Management’s (CoRWM) that the best available approach for the long-term management of higher activity radioactive waste is geological disposal, preceded by safe and secure interim storage.

In June 2008, following public consultation, the UK Government and devolved administrations for Wales and Northern Ireland published a White Paper, ‘Managing Radioactive Waste Safely: A Framework for Implementing Geological Disposal’10. This sets out a staged framework for implementing geological disposal based on voluntarism and partnership with local communities.

Following the White Paper, the Welsh Government reserved its position on the policy of geological disposal; however, it confirmed that it would continue to play a full part in the MRWS programme in order to ensure that the interests of Wales were taken into account. The Scottish Government does not support disposal of higher-activity wastes in a geological repository and is not directly engaged in the MRWS programme.

The UK Government is currently reviewing the site selection process elements of the MRWS programme, and intends to launch a public consultation in Autumn 2013 on how the process for implementing geological disposal might be improved.

The Organisation to deliver the Geological Disposal Facility in the UK is now part of the NDA and is known as the Radioactive Waste Management Directorate (RWMD), which was formed from Nirex(2). RWMD are continuing to do work on standards for the conditioning and packaging of radioactive waste for long-term management.

ONR oversees waste operations on nuclear licensed sites. The disposal of radioactive wastes may only be made under authorisations granted by the Environment Agency in England and Wales or in Scotland by the Scottish Environment Protection Agency (SEPA). This is done under operational agreements between the environment agencies and ONR.

2.8. Research and Development

2.8.1. R&D organisations

In the UK, nuclear energy is considered primarily an industrial matter and, as such, the majority of R&D funding comes from the private sector. Public sector spending comes through a range of channels including the NDA, the Research Councils and through direct commissioning from Government departments.

For applied research, the UK National Nuclear Laboratory (NNL) was created in 2008 by a merger of Nexia Solutions, originally operated by BNFL, with the British Technology Centre. The NNL operates as a government owned commercial enterprise and focuses much of its efforts on applied research with direct industrial uses, alongside technical consultancy services to government.

Government expenditure on nuclear R&D totalled 66 million pounds in 2010/2011 and in 2011/2012 Government committed to just under an additional 30 million pounds of funding (including 15 million pounds for a National Nuclear User Facility and 12.5 million pounds towards the construction of the international Jules Horowitz Research Reactor) In addition the NDA has spent 42.5 million pounds on R&D over the last four years and over the last five years Research Council investment in nuclear research and training has increased from 3 million pounds to 11.7 million pounds per year.

2.8.2. Development of advanced nuclear technologies

The Government has completed a programme of work looking at the UK’s Nuclear R&D capabilities. This programme of work formed the basis of the Nuclear Industrial Strategy published in March 2013 and included: a Landscape Review of current R&D; the development of a long-term energy strategy to 2050 and beyond; an industrial vision statement for the same period, and; a Nuclear R&D roadmap to 2050.

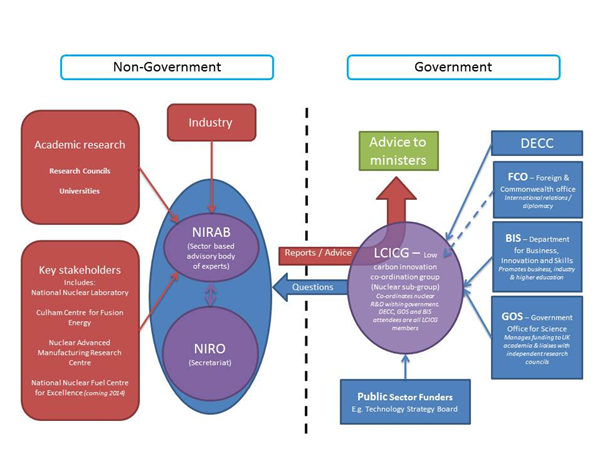

The UKs nuclear R&D capability is distributed across a wide range of public and private sector organisations, including universities, national labs and industrial partners. This landscape has driven the establishment of organisations to facilitate co-operation and long-term technology needs analysis. This includes the Nuclear Innovation and Research Advisory Board (NIRAB), which brings together representatives from sectors active in nuclear R&D in order to recommend future choices in R&D and the Nuclear Innovation and Research Office, which acts as the Board’s secretariat and liaises with Government on its behalf.

FIGURE 3. RELATIONSHIP BETWEEN GOVERNMENT AND NON-GOVERNMENT R&D SUPPORT STRUCTURES

2.8.3. International co-operation and initiatives

The UK is a member of the European Union (EU), the OECD/NEA and the IAEA as well as other bilateral and multilateral organizations. The UK Government supports EU programmes in the field of nuclear safety and nuclear waste management and participates in many OECD/NEA and IAEA projects.

The Nuclear Industrial Strategy also set out the Government’s intention to increase and improve its impact in international R&D fora.

2.9. Human resources development

As in other countries with a sizeable nuclear industry a large share of nuclear engineers in the UK are nearing retirement. Their knowledge and experience will be withdrawing from the highly specialised workforce at a time when the UK nuclear sector faces the double challenge of an ambitious target of new NPP construction and a large nuclear decommissioning programme. The Government has tried to anticipate and address the threat of skill shortages through the creation of a number of nuclear engineering programmes at universities, the Nuclear Skills Academy and the National Nuclear Laboratory. Responding to active Government encouragement, the universities of Birmingham, Lancaster and Manchester have added degree courses in nuclear engineering in recent years and student numbers are increasing. In the Nuclear Skills Academy, qualified “trainers” transmit the required knowledge for future employees of the nuclear industry, which are certified with the help of a Nuclear Skills Passport. The National Skills Academy for Nuclear is sponsored by the Nuclear Energy Skills Alliance, which brings together public and private actors to identify risks in the area of nuclear skills and recommend mitigating actions. The NDA launched its own Skills and Capability Strategy in 2008 with a budget of more than 40 million pounds.

2.10. Stakeholder Communication

The Government is working with those communities that have expressed an interest in possibly hosting a GDF. There has been extensive local public and stakeholder engagement in these areas where an interest has been shown. Government and NDA officials have participated in these and other engagements to explain Government policy and answer stakeholder questions and concerns.

The new nuclear programme has included numerous public consultations, and the UK Government also consults regularly with NGOs and local community groups through an NGO forum. The Government engages with the nuclear industry to do what is necessary to encourage commercial plans to come forward. Energy companies need to understand Government’s commitment, steps being taken to reduce risks, and the opportunities available to them. The Government also engages with the key consortia with plans for new nuclear in the UK through regular Challenge Meetings with individual companies, the Nuclear Industry Council, and regular Ministerial engagement.

3. NATIONAL LAWS AND REGULATIONS

3.1. Regulatory framework

3.1.1. Regulatory authority(s)

The Office for Nuclear Regulation (ONR) was established as an independent Public Corporation in April 2014, following legislation in the Energy Act 2013. ONR brings together the safety and security functions of HSE’s Nuclear Directorate, incorporating the Nuclear Installations Inspectorate, Office of Civil Nuclear Security and the UK Safeguards Office. Since October 2011, the ONR has also had responsibility for the regulation of transport of radioactive materials by road, rail and inland waterways, which were previously dealt with by the Department for Transport’s Radioactive Materials Transport Division (now part of the ONR). The Chief Nuclear Inspector, who also heads the ONR, has the power to issue, add conditions to, and revoke nuclear site licences.

Regulatory oversight for radiological protection rests with the Environment Agency in England, Natural Resources Wales(3), SEPA in Scotland, and the Northern Ireland Environment Agency in Northern Ireland. The Environment Agency oversees the implementation of the Environmental Permitting Regulations of 2010 (EPR10)11, which replace the Radioactive Substances Act of 199312(RSA 93) in England and Wales. RSA 93 remains in force in Scotland and Northern Ireland. The environment agencies oversee radioactive waste disposal at the UK’s nuclear sites, including site permits. They also regulate the storage and use of radioactive substances for non-nuclear users of radioactive materials such as hospitals and universities, while the ONR oversees the storage and use of radioactive substances at licensed nuclear sites. ONR and the environment agencies co-operate in fulfilling their respective missions.

Detailed information can be found on the respective websites of the UK’s regulatory bodies (see Appendix 2).

3.1.2. Licensing Process

The safety of UK nuclear installations, and the protection of employees and the public from the potential hazards caused by them, is governed principally by provisions in the Nuclear Installations Act 196513, the Health and Safety at Work etc. Act 197414, the Ionising Radiation Regulations 199915 made under it, EPR10 and RSA 93. No site may be used for the construction or operation of a commercial nuclear installation unless appropriate approval or planning permission has been given. The Nuclear Installations Act 1965 etc. (Repeals and Modifications) Regulations 197416 made the HSE the nuclear licensing authority for UK nuclear sites. These powers, to grant a licence or not and to attach conditions, are delegated to the post of the Chief Nuclear Inspector, ONR.

The creation of the NDA, in 2005, has not changed the regulatory framework outlined above.

The ONR will not grant a nuclear site licence unless satisfied that a prospective operator has the capacity to meet all their stringent safety requirements from design through to decommissioning, in adherence to the licence conditions attached to the site licence. So as to demonstrate to the ONR that safety will be properly controlled at all stages of the “lifecycle of plant” on licensed sites, the operator is required to produce a comprehensive written "safety case" for each plant. The safety case must be revised and updated throughout the plant's operation, to take account of any changes in its operating conditions, and a new safety case be similarly established and maintained for decommissioning.

Ultimate responsibility for the safety of a nuclear installation is legally the responsibility of the operating company. They must execute all licence requirements to the ONR’s satisfaction. The principle is the same whether the operating company is in the public or private sector. The ONR carefully monitors the performance of nuclear installations against exacting standards and conditions. Should there be any doubt about a licensee's continued ability to meet its obligations, the ONR has extensive powers. They can, for example, include additional licence conditions at any time, direct the cessation of plant operation, and ultimately direct that it be shut down altogether. An operating company may surrender a licence (or it may be revoked by the ONR), but still retains responsibility for safety of the site until either a new licence for the site is issued or the HSE is satisfied that there ceases to be a danger from ionising radiation from the site.

EPR10 and RSA93 makes the Environment Agency the regulatory body for authorisation for the disposal of radioactive waste in respect of nuclear licensed sites in England and Wales and SEPA the regulatory body for Scotland, respectively. As part of the Basic Safety Standards Directive 96/29/Euratom17 a number of the environment agencies’ existing administrative practices under RSA 93 were made legally binding obligations.

There is close liaison between ONR, the Environment Agency and SEPA under the terms of Memoranda of Understanding, which set out the lead roles of the organisations and requirements for liaison and consultation.

As far as security regulation is concerned, nuclear power stations and associated laboratories are regulated separately under the Nuclear Generating Stations (Security) Regulations 199618.

The Nuclear Industries Security Regulations 200319, provides a single, clarified and updated legislative basis for security regulation of those holding nuclear material and sensitive nuclear information, and introduced direct regulation of those transporting nuclear material.

3.2. Main national laws and regulations in nuclear power

Nuclear Installations

Atomic Energy Act 1946 (Chapter 80)

Atomic Energy Act 1988 (Chapter 7)

Atomic Energy (Miscellaneous Provisions) Act 1981 (Chapter 48)

Atomic Energy Authority Act 1954 (Chapter 32)

Atomic Energy Authority Act 1971 (Chapter 11)

Atomic Energy Authority Act 1986 (Chapter 3)

Atomic Energy Authority Act 1995 (Chapter 37)

Energy Act 1983 (Chapter 25)

Energy Act 2004

Energy Act 2008

Health and Safety at Work etc Act 1974 Chapter 7

Ionising Radiations Regulations 1999 (SI 1999/3232).

Nuclear Installations Act 1965 (Chapter 57)

Nuclear Installations (Amendment) Act 1965 (Chapter 6)

Nuclear Installations Act 1969 (Chapter 18)

Nuclear Industry (Finance) Act 1977 (Chapter 7)

Utilities Act 2000

Air Navigation (Restriction of Flying) (Nuclear Installations) Regulations 1988 (SI 1988/1138)

Fire Certificate (Special Premises) Regulations 1976 (SI 1976/2003)

Nuclear Decommissioning and Waste Handling (Finance and Fees) Regulations 2011

Nuclear Generating Stations (Security) Regulations 1996

Nuclear Installations Act 1965 etc. (Repeals and Modifications) Regulations 1974 (SI 1974/2056)

Nuclear Installations Act 1965 (Repeal and Modifications) Regulations 1990 (SI 1990/1918)

Nuclear Installations (Dangerous Occurrences) Regulations 1965 (SI 1965/1824)

Nuclear Installations (Insurance Certificate) (Amendment) Regulations 1969 (SI 1969/64)

Nuclear Installations Regulations 1971 (SI 1971/1381)

Nuclear Installations (Expected Matter) Regulations 1978 (SI 1978/1779)

Nuclear Installations (Prescribed Sites) Regulations 1983 (SI 1983/919)

The Notification of Installations Handling Hazardous Substances Regulations 1982 (SI 1982/1357)

The Public Information for Radioactive Emergencies Regulations 1992 (SI 1992/2997)

Radiation (Emergency Preparedness and Public Information) Regulations 2001, SI 2001 No. 2975

The Atomic Energy (Mutual Assistance Convention) Order 1990 (SI 1990/235)

The Justification Decision (Generation of Electricity by the AP1000 Nuclear Reactor) Regulations 2010, and The Justification Decision (Generation of Electricity by the EPR Nuclear Reactor) Regulations 2010.

Health Protection Agency Act 2004

Freedom of Information (FOI) Act 2000

Town and Country Planning Act 1990

The Planning (Hazardous Substances) Regulations 1992

Town and Country Planning (Scotland) Act 1997

The Planning etc (Scotland) Act 2006

The Planning Act 2008

Environmental Protection

Radiological Protection Act 1970 (Chapter 46)

Environmental Protection Act 1990 (Chapter 43)

Radioactive Substance Act 1993 (Scotland and Northern Ireland) (Chapter 12)

Environment Act 1995

Control of Pollution (Radioactive Waste) Regulations 1976 (SI 1976/959)

Control of Pollution (Radioactive Waste) Regulations 1989 (SI 1989/1158)

Environmental Protection (Prescribed Processes and Substances) (Amendment) Regulations 1992 (SI 1991/614)

Environmental Permitting (England and Wales) Regulations 2010 (SI 2010/675) (Schedule 23)

Environmental Permitting (England and Wales) (Amendment) Regulations 2011 (SI 2011/2043)

Justification of Practices Involving Ionising Radiation Regulations 2004 (SI 2004/1769)

Nuclear Reactors (Environmental Impact Assessment for Decommissioning) Regulations 1999 (SI 1999/2892)

Nuclear Reactors (Environmental Impact Assessment for Decommissioning) Regulations 2006

Radioactive Substances (Records of Convictions) Regulations 1992 (SI 1992/1685)

Environmental Protection Act 1990 (Commencement No 3) Order 1990 (SI 1990/2565 (Chapter 67))

Environment Protection Act 1990 (Commencement No 7) Order 1991 (SI 1991/1042)

Security

Anti-Terrorism, Crime and Security Act 2001

Nuclear Industries Security Regulations 2003

Nuclear Material (Offences) Act 1983 (Commencement) Order 1991 (SI 1991/1716)

Extradition (Protection of Nuclear Material) Order 1991 (SI 1991/1720)

Nuclear Installations (Application of Security Provisions) Order 1993 (SI 1993/687)

General

Criminal Justice Act 1982

Criminal Law Act 1989

Electricity Act 1989

The Exports of Goods (Control) Order 1992 (SI 1992/3092)

The National Radiological Protection Board (Extension of Functions) Order 1974 (SI 1974/1230)

Transport

Radioactive Material (Road Transport) Act 1991 (Chapter 27)

Radioactive Material (Road Transport) (Great Britain) Regulations 1996

Transfrontier Shipment of Radioactive Waste and Spent Fuel Regulations 2008

Carriage of Dangerous Goods and Use of Transportable Pressure Equipment Regulations 2009 (as amended 2011)

Defence

Atomic Weapons Establishment Act 1991 (Chapter 46)

REFERENCES

‘Meeting the Energy Challenge – A White Paper on Nuclear Power’, Cm 7296, January 2008, http://www.berr.gov.uk/files/file43006.pdf

Japanese earthquake and tsunami: Implications for the UK Nuclear Industry, Interim Report, HM Chief Inspector of Nuclear Installations, 18 May 2011, http://www.hse.gov.uk/nuclear/fukushima/index.htm

Japanese earthquake and tsunami: Implications for the UK nuclear industry Final Report., http://www.hse.gov.uk/nuclear/fukushima/index.htm

European Council “Stress Tests” for UK nuclear power plants – National Final Report. http://www.hse.gov.uk/nuclear/news/2012/jan-stress-test-report.htm

NDA Strategy, Effective from April 2011,.http://www.nda.gov.uk/documents/upload/NDA-Strategy-Effective-from-April-2011-full-colour-version.pdf

Energy Act 2008, http://www.legislation.gov.uk/ukpga/2008/32/pdfs/ukpga_20080032_en.pdf

Funded Decommissioning Programme Guidance for New Nuclear Power Stations, http://www.gov.uk/government/organisations/department-of-energy-climate-change

Planning our Electric Future: A White Paper for Secure, Affordable and Low-Carbon Electricity, http://www.gov.uk/government/organisations/department-of-energy-climate-change

National Policy Statement for Nuclear Power Generation, https://www.gov.uk/government/publications/national-policy-statements-for-energy-infrastructure

Managing Radioactive Waste Safely: A Framework for Implementing Geological Disposal, White Paper, Defra, BERR and the devolved administrations for Wales and Northern Ireland, June 2008,http://mrws.decc.gov.uk/

Environmental Permitting (England and Wales) Regulations 2010 (EPR10), April 2010, http://www.defra.gov.uk/environment/policy/permits/guidance.htm

Radioactive Substances Act 1993, http://www.opsi.gov.uk/ACTS/acts1993/Ukpga_19930012_en_1.htm

Nuclear Installations Act 1965 (as amended) (1965 c.57), http://www.statutelaw.gov.uk/Home.aspx

Health and Safety at Work etc. Act 1974 (1974 c.37), http://www.hse.gov.uk/legislation/hswa.pdf

The Ionising Radiations Regulations 1999, http://www.opsi.gov.uk/si/si1999/19993232.htm

The Nuclear Installations Act 1965 etc. (Repeals and Modifications) Regulations 1974, http://www.legislation.gov.uk/uksi/1974/2056/contents/made

96/29/Euratom - Basic Safety Standards for radiation protection, 1996, Official Journal of the European Communities (1996) 39, No. L159, http://ec.europa.eu/energy/nuclear/radioprotection/doc/legislation/9629_en.pdf

Nuclear Generating Stations (Security) Regulations 1996, http://origin-www.legislation.gov.uk/uksi/1996/665/contents/made

Nuclear Industries Security Regulations 2003, http://www.legislation.gov.uk/uksi/2003/403/part/1/made

APPENDIX 1: INTERNATIONAL, MULTILATERAL AND BILATERAL AGREEMENTS

International treaties, conventions & agreements

| Agreement on privileges and immunities of the IAEA | Entry into force: | 19 September 1961 |

| Convention on Nuclear Safety | Ratified: Entry into force: | 17 January 1996 24 October 1996 |

| Joint Convention on the Safety of Spent Fuel Management and on the Safety of Radioactive Waste Management | Ratified: Entry into force: | 20 September 1994 18 June 2001 |

| Convention on the Early Notification of a Nuclear Accident | Ratified: Entry into force: | 9 February 1990 12 March 1990 |

| Convention on Assistance in the Case of a Nuclear Accident of Radiological Emergency | Ratified Entry into force: | 9 February 1990 12 March 1990 |

| Convention on the Prevention of Marine Pollution by Dumping of Wastes and other Matter (London Convention) 1996 Protocol to the London Convention | Entry into force: Contracting Party Ratified: Entry into force: | 1975 15 December 1998 24 March 2006 |

| Convention on the Physical Protection of Nuclear Material Amendment to the Convention on the Physical Protection of Nuclear Material | Ratified: Entry into force: Ratified: | 6 September 1991 6 October 1991 8 April 2010 |

| OSPAR Convention for the Protection of the Marine Environment of the North-East Atlantic | Entry into force: Contracting Party | 25 March 1998 |

| Convention relating to civil liability in the field of maritime carriage of nuclear materials | Entry into force: | 15 July 1975 |

| United Nations Convention on the Law of the Sea | Entry into force: UK Accession: | 16 November 1994 25 July 1997 |

| ESPOO Convention | Signatory: Ratification: | 26 February 1991 10 October 1997 |

| Aarhus Convention | Signatory: Ratification: | 25 June 1998 23 February 2005 |

| Vienna Convention on Civil Liability for Nuclear Damage | Signatory: | 11 November 1964 |

| Paris Convention on Third Party Liability in the Field of Nuclear Energy | Ratified: | 23 February 1966 |

| Brussels Convention on Supplementary Compensation | Ratified: | 24 March 1966 |

| Joint Protocol Relating to the Application of the Vienna Convention and the Paris Convention | Signatory: | 21 September 1988 |

| EURATOM Treaty | Member State |

Co-operation agreements with IAEA and bilateral agreements with other countries in area of Nuclear Power

The UK is member of OECD/NEA and its standing committees and is fully involved in the IAEA’s work on safety, security, safeguards and nuclear energy. The following are current safeguards agreements with the IAEA:

Agreement between the Agency and the United Kingdom of Great Britain and Northern Ireland for the Application of Safeguards. Entry into force: 14 December 1972. Published by IAEA as INFCIRC/175.

Agreement of 6 September 1976 between the United Kingdom of Great Britain and Northern Ireland, the European Atomic Energy Community and the Agency in connection with the Treaty on the Non-Proliferation of Nuclear Weapons. Entry into force: 14 August 1978. Published by IAEA as INFCIRC/263.

Protocol Additional to the agreement at (2) above, also known as the ‘UK Additional Protocol’. Entry into force: 30 April 2004. Published by IAEA as INFCIRC/263/Add.1.

The UK has bilateral agreements with France, Japan, Ireland and the Netherlands. It also has civil nuclear cooperation agreements as follows:

| Country | Year Signed | Entry into force |

| China | 1985 | 3 June 1985 |

| Japan | 1998 | 12 October 1998 |

| Jordan | 2009 | |

| Korea, Republic of | 1991 | 27 November 1991 |

| Russian Federation | 1996 | 3 September 1996 |

| United Arab Emirates | 2010 | |

| USA | 1955 | 21 July 1955 |

ONR has Information Exchange Arrangements with overseas nuclear safety regulators in Canada, Finland, France, Ireland, South Africa and the USA, and, agreements with Technical Support Organisations in Finland, France, Germany and the USA. More information can be found on the HSE website at:

www.hse.gov.uk/nuclear/operational/research/gres013.htm#app1

As a Member State of the European Union, the UK is party, through its membership of the EURATOM community, to various agreements with third countries.

APPENDIX 2: MAIN ORGANISATIONS, INSTITUTIONS AND COMPANIES INVOLVED IN NUCLEAR POWER RELATED ACTIVITIES

Name of report coordinator:

Ms Frankie Brookes-Tombs

Institution:

EU and International Policy for Nuclear Safety

And Radioactive Waste Management

M06

55 Whitehall

London

SW1A 2EY

Contacts:

Tel.: + 44 300 068 6115

Email: frankie.brookes@decc.gsi.gov.uk